Have you been a loyal fan of NHIF but now find yourself in limbo as the government looks to shift to SHIF? You’re not alone! It’s like Kenya’s healthcare system is getting a makeover, and we’re all wondering if it’s going to be a glow-up or just a new haircut.

NHIF, the reliable old friend that’s been with us for 57 years, is about to be replaced by the new kid on the block, SHIF. Will it be better? Or will you be left longing for the good old days? What will be the difference? What’s the structure of the new contributions?

Don’t worry; this article is about to answer all your questions, and more!

Also Read: What is SHIF and How to Register for SHA

What is Social Health Insurance Fund (SHIF)?

First things first! What exactly is this SHIF?

The Social Health Insurance Fund (SHIF) is a new healthcare initiative introduced by President William Ruto’s administration in Kenya, aimed at providing affordable and accessible healthcare to all citizens. This program is set to replace the National Health Insurance Fund (NHIF), which has been in operation for 57 years.

SHIF represents a significant shift in Kenya’s healthcare landscape. Unlike NHIF, which primarily served employed individuals, SHIF aims to be more inclusive by covering those in the informal sector and unemployed citizens who were previously left out. This aligns with Kenya’s constitutional mandate to provide appropriate healthcare services to all.

NHIF vs SHIF Contributions

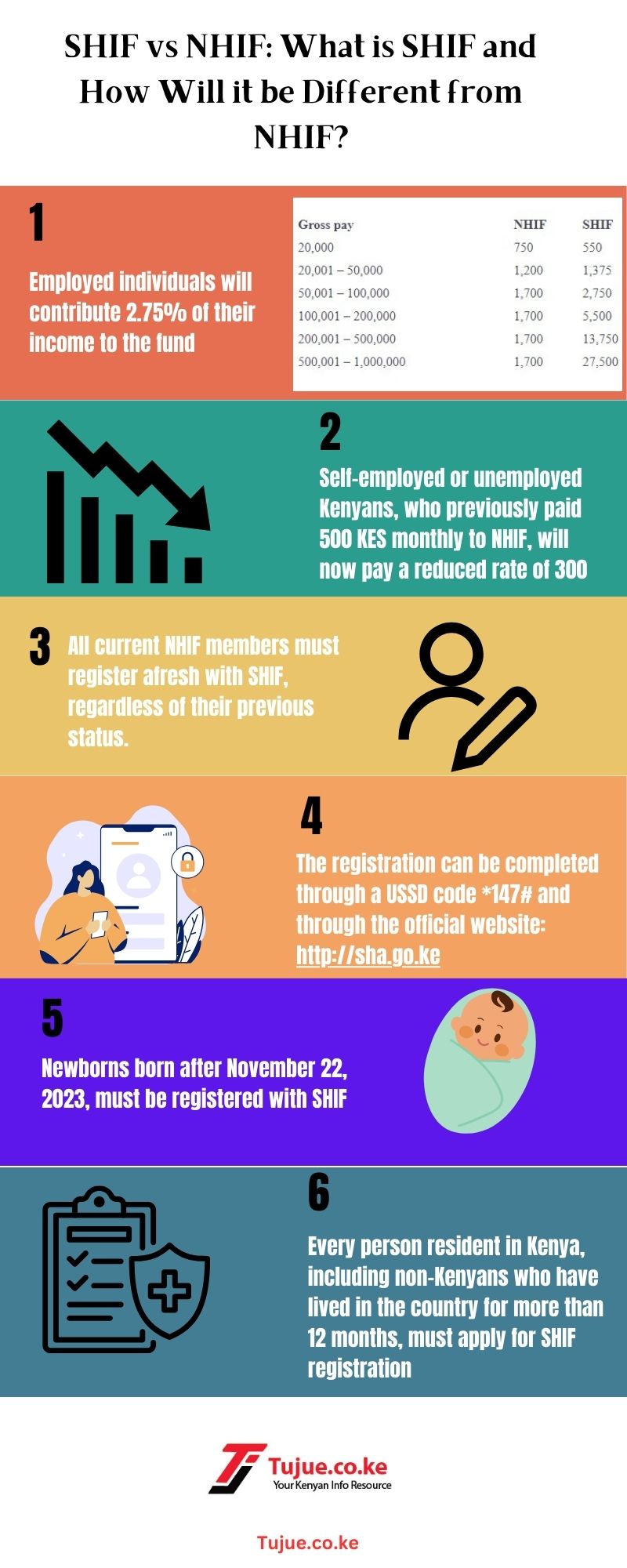

Under SHIF, employed individuals will contribute 2.75% of their income to the fund. The government will cover contributions for those unable to pay, ensuring universal coverage.

Self-employed or unemployed Kenyans, who previously paid 500 KES monthly to NHIF, will now pay a reduced rate of 300 KES under a graduated system based on their ability to contribute.

The new system promises to offer a comprehensive range of healthcare services across various medical fields, providing holistic coverage to all Kenyans.

| Gross pay | NHIF | SHIF |

|---|---|---|

| 20,000 | 750 | 550 |

| 20,001 – 50,000 | 1,200 | 1,375 |

| 50,001 – 100,000 | 1,700 | 2,750 |

| 100,001 – 200,000 | 1,700 | 5,500 |

| 200,001 – 500,000 | 1,700 | 13,750 |

| 500,001 – 1,000,000 | 1,700 | 27,500 |

Benefits of SHIF over NHIF

SHIF’s implementation is set to have far-reaching impacts on Kenya’s healthcare system and society at large. As the country transitions from NHIF to this new model, several key areas are expected to undergo significant changes.

From the cost of healthcare and access to services, to the quality of medical care and the operations of businesses, these impacts will affect individuals, businesses, and the overall healthcare infrastructure.

Here’s what to expect:

1. Cost of Healthcare

SHIF aims to create a more equitable healthcare system by implementing a graduated contribution scale. Lower-income individuals will pay reduced rates or access free care.

For instance, self-employed or unemployed Kenyans who previously paid 500 KES monthly to NHIF will now pay only 300 KES under SHIF. The government will cover contributions for those unable to pay, ensuring universal coverage.

However, higher earners will see a notable increase in their contributions. The new system requires a 2.75% deduction from gross salary for employed individuals.

For example, someone earning 500,000 KES monthly would contribute approximately 13,750 KES to SHIF, which could be a substantial increase from their previous NHIF contributions.

2. Access to Services

SHIF plans to expand healthcare access by creating a comprehensive primary care network. This network will include not only public healthcare facilities but also private hospitals accredited by the Social Health Authority (SHA).

This diverse network aims to ensure that Kenyans can access healthcare services closer to their locations and with reduced wait times.

3. Healthcare Quality

The increased funding pool from SHIF is expected to lead to substantial improvements in healthcare quality across the country. This additional funding could be directed towards:

- Upgrading existing healthcare facilities with modern equipment and technologies

- Improving the supply chain for medicines and medical supplies, reducing shortages

- Investing in training and development for healthcare professionals

- Implementing advanced medical technologies and treatments previously unavailable in many parts of the country

- Enhancing preventive care programs and public health initiatives

Disadvantages of SHIF Over NHIF

While the Social Health Insurance Fund (SHIF) aims to improve healthcare access and equity in Kenya, it’s important to recognize that this transition from the National Health Insurance Fund (NHIF) may present certain challenges and disadvantages.

These drawbacks could affect various stakeholders, including individuals, businesses, and the healthcare sector itself.

According to health CS Susan Nakhumicha:

“The transition committee needs to make a formal submission and proposal for addressing issues in the alternative plan due to the identified factors that are not ready for July 1 and this includes staggered implementation of the benefits package among others. This will imply communication methodologies including who will make such communications”

Let’s look at some of the potential disadvantages of SHIF compared to the existing NHIF system:

1. Increased Financial Burden on Higher Earners

Under SHIF, the contribution rate of 2.75% of gross salary could significantly increase the financial burden on higher-earning individuals compared to the NHIF’s capped contribution system.

For instance, an individual earning more than 500,000 KES monthly would contribute 27,500 KES to SHIF, which is much more than their previous NHIF contribution.

2. Complex Transition Process

The shift from NHIF to SHIF requires a comprehensive re-registration process for all Kenyans, including current NHIF members. This transition could be time-consuming and confusing for many citizens, especially those in rural or underserved areas who may have limited access to information or registration facilities.

3. Initial Implementation Challenges

As with any new system, SHIF may face teething problems during its initial implementation. These could include technical glitches in the registration process, delays in setting up the new administrative structure, and confusion among healthcare providers about the new procedures and coverage details.

4. Impact on Businesses

The introduction of SHIF will have multifaceted effects on businesses in Kenya:

- Increased Operational Costs

Companies will need to adjust their payroll systems to accommodate the new 2.75% SHIF deduction, requiring software updates or new systems. This could be particularly challenging for small and medium-sized enterprises with limited resources.

- Compliance Burdens

Businesses may need to invest in training for HR and finance staff to ensure proper implementation of SHIF regulations. They might also need to hire SHIF experts or consultants for compliance, adding to their operational expenses.

Transition from NHIF to SHIF and Registration

The Kenyan government decided to delay the implementation of the Social Health Insurance Fund (SHIF), pushing the launch date to October 1st, 2024.

This came as a result of several ongoing issues, particularly with the development of the digital infrastructure required to support the new system. Additionally, there are still legislative matters that need to be addressed before SHIF can be fully operational.

In the meantime, Kenyan citizens continue to make their health insurance contributions to the existing National Health Insurance Fund (NHIF), even with the scandals it continues to face.

The shift from NHIF to SHIF requires a comprehensive re-registration process:

- All current NHIF members must register afresh with SHIF, regardless of their previous status.

- The registration can be completed through a USSD code *147# and through the official website: http://sha.go.ke

- SHIF registration process completely free

- Every person resident in Kenya, including non-Kenyans who have lived in the country for more than 12 months, must apply for SHIF registration.

- Newborns born after November 22, 2023, must be registered with SHIF

- The registration process is expected to be digital, requiring individuals to provide personal information, employment details, and choose their preferred healthcare providers from the SHIF network.

- SHIF allows contributors to include their spouse and children under 25 as beneficiaries.

Key Takeaway

SHIF represents a bold step towards universal healthcare coverage in Kenya, addressing many of the limitations of the previous NHIF system. While it presents some challenges, particularly for higher earners and businesses, it promises to significantly improve healthcare access and quality for a broader segment of the Kenyan population.

What is left is to see if the government will push through with the implementation of SHIF and how smoothly it will be rolled out.